Top Guide to Understanding Florida Reverse Mortgages

Wondering about a Florida reverse mortgage? If you’re a homeowner aged 62 or older, this financial option lets you turn your home equity into cash. Florida’s large retiree community makes this especially beneficial here. This guide will explain how Florida reverse mortgages work, their benefits, and who is eligible.

Key Takeaways

Reverse mortgages enable seniors aged 62 and older to convert home equity into cash without selling their homes or making monthly payments, providing financial flexibility during retirement.

Eligibility for reverse mortgages in Florida requires homeownership, the property being a primary residence, and the borrower being at least 62 years old, while also maintaining responsibility for taxes, insurance, and home repairs.

Repayment of reverse mortgages occurs upon the homeowner’s death, sale of the home, or permanent move, with non-recourse provisions protecting heirs from owing more than the home’s value.

What is a Reverse Mortgage?

How Reverse Mortgages Work in Florida

Reverse mortgages have found significant popularity among Florida homeowners, a demographic heavily populated with retirees. For such loans to be granted, the borrower’s primary residence must act as the security for the lender. As an advantage of reverse mortgages, while you continue living in your home, there is no requirement to make any monthly payments.

The Federal Housing Administration (FHA) plays a crucial role in setting limits and regulations for reverse mortgages. It is imperative for those holding reverse mortgages in Florida to keep up-to-date with property taxes and homeowner’s insurance premiums, alongside other financial responsibilities like upkeep costs or Homeowners’ Association (HOA) fees. Should these not be maintained promptly, it could result in lenders using loan proceeds to cover such expenses or demand immediate repayment of the loan.

The debt incurred from a reverse mortgage does not fall due until the death of all borrowers on title or when they vacate their home permanently. Upon one of these events occurring, disposal of the estate property can settle what’s owed on this form of lending arrangement. Notably though, if revenue generated from selling said residence fails to meet total outstanding amount owed on mortgage balance. Heirs remain protected against personal liability for any remaining deficiency ensuring their financial safeguarding.

Reverse mortgages allow individuals 62 years or older to tap into their home’s equity, converting it into cash while maintaining homeownership and forgoing the requirement of monthly mortgage payments. This financial instrument can be pivotal in enhancing retirees’ income streams, covering healthcare expenditures, or improving overall quality of life.

Unlike traditional mortgages that require borrowers to remit monthly payments toward their loan balance, a reverse mortgage reverses this flow. The lender disburses funds to the homeowner using the property as security. Consequently, homeowners continue living in their residences without being burdened by monthly payments.

The funds garnered from a reverse mortgage come with versatile disbursement options: they may arrive as one lump sum payment, regular monthly installments, or accessible through a line of credit—all typically devoid of tax obligations. Homeowners often utilize these resources for various necessities such as paying off medical expenses, funding house maintenance work, or simply managing day-to-day costs—and repayment is deferred until after death occurs—leaving heirs responsible—the borrower permanently relocates elsewhere or opts to sell their domicile.

Eligibility Criteria for Florida Reverse Mortgages

To qualify for a reverse mortgage in Florida and utilize your home’s equity, borrowers must meet the following criteria:

Be at least 62 years old.

The home must be their primary residence.

They should either own the home outright or have a low mortgage balance that can be paid off at closing.

Homeowners must maintain their property, pay property taxes, and keep up with homeowner’s insurance. Eligible property types include single-family homes, townhouses, and condominiums, making the product accessible to many homeowners.

What Type of Homes Qualify for a Reverse Mortgage?

To qualify for a reverse mortgage, your home must meet specific criteria. Florida eligible properties include single-family homes, 2-4 unit homes with the borrower occupying one unit, HUD-approved condominium projects, and FHA-compliant manufactured homes. It’s crucial that the home adheres to FHA property standards and flood requirements to ensure safety and compliance.

Additionally, the home must serve as the borrower’s primary residence, meaning you need to live in the home for at least six months of the year. This residency requirement ensures that the property remains your main living space, which is a key condition for maintaining the reverse mortgage.

Types of Reverse Mortgages Available

In Florida, there are three main types of reverse mortgages designed to cater to diverse financial requirements. The Home Equity Conversion Mortgage (HECM) is the most prevalent type and comes with federal insurance, enabling elderly homeowners to transform their home equity into liquid assets. HECMs can be utilized for purchasing a new residence without the obligation of monthly mortgage payments.

Private lenders offer proprietary reverse mortgages which provide access to a greater portion of home equity than HECMs do. This can be particularly advantageous for owners of higher-value homes.

Local government entities or non-profit organizations exclusively provide single-purpose reverse mortgages intended for particular uses such as funding property taxes or conducting home repairs.

Reverse mortgage eligibility in Florida encompasses various dwelling types including single-family houses, condominiums, townhouses, and some categories of manufactured homes. Thereby presenting numerous options concerning property types.

Benefits of Reverse Mortgages in Florida

Reverse mortgages provide a substantial advantage for seniors aiming to bolster their financial security and optimize their retirement funds. This type of arrangement ensures that the money received is not taxed, which can substantially enhance retirees’ economic stability without imposing additional tax liabilities on them.

By engaging in reverse mortgages, homeowners retain complete ownership rights over their properties and may remain living there as it remains their primary residence. This continuity provides significant comfort and assurance. When the homeowner passes away, any outstanding balance due on the reverse mortgage is settled through the home’s equity. This measure safeguards heirs from shouldering any debt burden.

Florida residents benefit from the adaptability offered by reverse mortgages when it comes to tapping into home equity because they are given an avenue to augment their income during retirement years. Such flexibility proves useful for meeting unplanned expenses or simply improving one’s lifestyle after retiring from active employment.

How Much Can You Borrow with a Reverse Mortgage?

Your borrowing capability with a reverse mortgage is determined by factors such as the age of the youngest borrower, your home’s appraised value, and prevailing interest rates. A more senior borrower typically qualifies for a higher loan amount, while homes with greater value can increase available funds. While reverse mortgage calculators offer approximations, to acquire exact figures it’s imperative you speak with an officer who specializes in reverse mortgage loans.

In terms of Florida specifically, reverse mortgages See an average loan size around $125,000. This figure fluctuates considerably depending on personal situations. To gain insight into what you personally qualify for regarding a reverse mortgage loan amount, seeking advice from a professional in the field is recommended.

How to Use Reverse Mortgage Proceeds

The versatility of reverse mortgages is a significant draw, providing recipients with multiple options for receiving their funds. Individuals can opt for a lump sum payment, establish monthly payments, access a line of credit, or employ some combination thereof. A reverse mortgage line is a flexible financial option that allows borrowers to take out funds as needed, with interest only paid on the utilized amount. This flexibility allows older adults to design a financial plan that aligns with their personal requirements and lifestyle choices.

Using proceeds from reverse mortgages can serve an array of needs such as funding home improvements, managing everyday living costs, settling medical expenses, or underwriting the costs associated with long-term care. The additional income stream these loans provide plays an important role in enhancing retirement finances and alleviating other monetary pressures.

Freedom surrounds the application of funds acquired through reverse mortgages. There are no rigid stipulations governing their use. This provides retirees with the latitude to address various financial demands as they surface—whether it’s keeping up property upkeep standards, taking care of health-related outlays or simply indulging in recreational pursuits—the benefits from reverse mortgage advances ensure adjustable economic support during one’s golden years.

Disbursement Options

Reverse mortgage funds offer flexibility in how you receive and use the proceeds, catering to various financial needs and preferences. Here are the three main disbursement options available:

Single Disbursement Lump Sum

With the single disbursement lump sum option, you receive the entire loan amount in one payment at closing. This can be particularly beneficial if you need a substantial amount of money upfront, such as to pay off an existing mortgage or cover a significant expense. It provides immediate access to a large sum, allowing you to address pressing financial needs.

Line of Credit

A line of credit offers the flexibility to draw on the loan amount as needed, up to a predetermined limit. This option is ideal for those who want to have funds available for future expenses or emergencies. One of the key advantages is that you only pay interest on the amount you actually borrow, and the unused portion of the line of credit can grow over time, providing a financial cushion for the future.

Term Payment

With term payments, you receive equal monthly payments for a set period, which can range from a few years to several decades. This option provides a steady income stream, making it useful for supplementing retirement income or covering ongoing living expenses. The payment amount is determined by factors such as your age, the loan amount, and the interest rate.

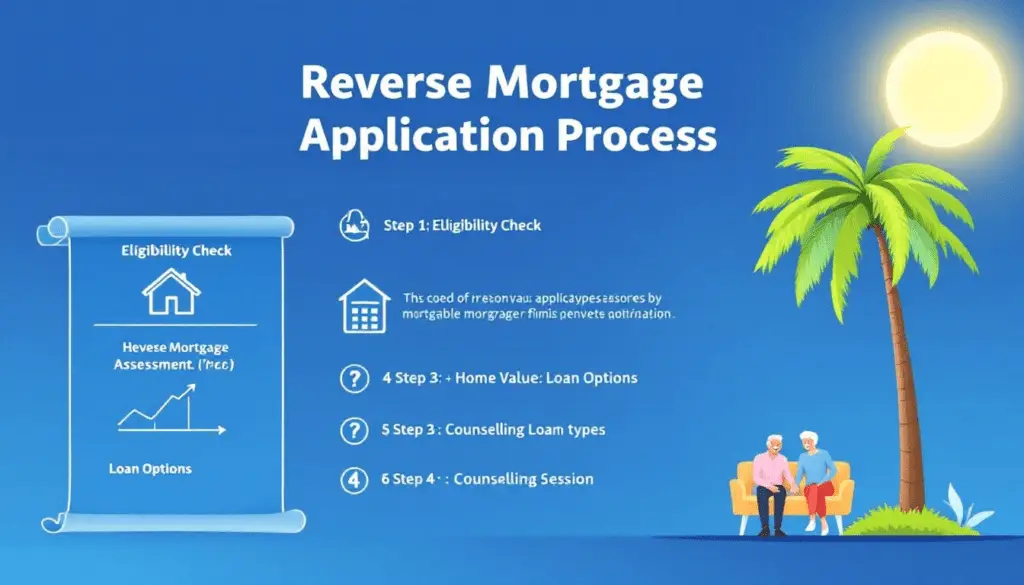

The Reverse Mortgage Application Process

Engaging in the process of securing a reverse mortgage requires adherence to certain procedural measures designed to promote educated choices. An indispensable initial measure is taking part in a counseling session conducted by an agency sanctioned by HUD, with the aim of imparting comprehensive knowledge about the nature and consequences of opting for a reverse mortgage.

Subsequent to this advisory encounter, applicants are required to submit their formal application, facilitate an appraisal of their property’s value, and undergo financial scrutiny. In assessing eligibility criteria such as credit standing, income levels, and asset possession durations ranging from 30-45 days may be expended by lenders reviewing these factors.

Experts trained in navigating the intricacies of reverse mortgages offer invaluable assistance during this procedure. They play an instrumental role in dispelling any ambiguities that arise while ensuring all pertinent paperwork is meticulously prepared. It is crucial for individuals venturing into such agreements to gain insight into associated expenditures — including but not limited to origination fees, ongoing service costs and premiums payable on mortgage insurance policies.

Repayment of Reverse Mortgage Loans

Repayment of a reverse mortgage is triggered when the last borrower sells the home, moves out, or passes away. At this point, the loan balance becomes due, and the estate can sell the home to repay the mortgage. The non-recourse feature ensures the estate is not responsible for any remaining debt if the home sells for less than the loan balance.

Heirs have options for repaying the reverse mortgage: selling the home, refinancing the balance, or paying off the loan with other funds. They are not personally liable for the debt, as repayment is tied to the home, not the borrower’s estate.

To avoid foreclosure, homeowners must maintain their property and stay current on property taxes and insurance. In some cases, borrowers can provide a deed in lieu of foreclosure to the lender to avoid foreclosure proceedings.

Protections and Rights for Borrowers

Reverse mortgages are equipped with numerous safeguards for borrower protection, being loans under stringent government regulation. An essential safeguard is the non-recourse clause, which guarantees that neither borrowers nor their heirs will be responsible for paying more than the home’s worth should the loan balance exceed its appraised value.

Borrowers retain the option to rescind their reverse mortgage contract within three days post-closing, allowing them a buffer period in case they reconsider. Surviving spouses have been granted assurance. They can stay in the residence without needing to repay immediately if specific prerequisites are fulfilled, offering Stability for families.

To avoid unforeseen repayment challenges, it’s crucial that borrowers communicate clearly with their heirs about a reverse mortgage’s specifics. The government persists in fortifying these safety measures and regulations so as to ensure that seniors have access to secure financial choices through reverse mortgages.

Common Myths About Reverse Mortgages

There are several misunderstandings about reverse mortgages that dissuade homeowners from considering them. It’s falsely believed by some that the loan amount could exceed the value of their home, but this risk is mitigated by federal insurance. There is also a misconception that lenders assume ownership of the property when in fact, homeowners maintain ownership provided they adhere to loan conditions.

Contrary to popular belief, reverse mortgages do not require monthly mortgage payments. As long as borrowers fulfill their responsibilities associated with maintaining the property and paying taxes and insurance, no monthly payments need to be made. It is possible for a homeowner to sell a house even if it has a reverse mortgage attached without facing any penalties for settling early.

Misconceptions like these often arise from insufficient knowledge surrounding reverse mortgages. Through proper education on how these financial products work, homeowners can come to understand and appreciate the potential advantages offered by reverse mortgages.

Reverse Mortgage Loans: Unlocking Home Equity for Seniors

A reverse mortgage loan is a financial tool designed to help seniors leverage their home equity for improved cash flow during retirement. In states like Florida, often referred to as the “Sunshine State,” this type of loan has gained popularity for its potential to empower older homeowners. A common type of reverse mortgage loan is the Home Equity Conversion Mortgage (HECM loan), a federally insured product that enables homeowners aged 62 or older to convert their equity into monthly payments, lump sums, or a line of credit. These reverse mortgage proceeds can be used for any purpose, from paying off an existing mortgage to covering living expenses or medical costs. Borrowers work closely with a loan officer to determine their eligibility and establish the principal limit—the maximum amount they can borrow, influenced by factors such as interest rates and the home’s appraised value.

For couples, a reverse mortgage in Florida can provide added security, as provisions are available to ensure a surviving spouse can remain in the home if one spouse passes away. However, it is crucial to understand the loan’s terms. If the borrower dies, the loan must typically be repaid through the sale of the home unless additional funds are available to settle the balance. This arrangement allows seniors to enjoy financial stability without immediate repayment obligations, helping them thrive in retirement. By tapping into their equity through a HECM loan, seniors in the Sunshine State can relieve financial burdens, eliminate existing mortgages, and sustain a more comfortable lifestyle. A reverse mortgage loan isn’t just a financial strategy—it’s a way of helping seniors maintain independence and peace of mind.

Summary

To summarize, reverse mortgages present a reliable and adaptable option for elderly residents of Florida to tap into their home equity, bolstering their financial well-being during their golden years. Homeowners have the choice among various types like HECMs, proprietary reverse mortgages, or single-purpose options to match with their unique requirements. The tax-free nature of the funds obtained from such arrangements, coupled with maintaining ownership rights over one’s property and protection under non-recourse terms, contribute greatly toward ensuring comfort and security.

For senior homeowners in the Sunshine State pondering over securing a reverse mortgage, this could prove to be an astute fiscal strategy. This avenue offers access to sustained financial serenity by eliminating the need for monthly mortgage payments throughout your time of leisure post-retirement. Seeking guidance from an expert in reverse mortgages is recommended so you can review what’s available thoroughly and take action that best aligns with your long-term financial aspirations.

Frequently Asked Questions

What is a reverse mortgage?

A reverse mortgage is a financial product designed for homeowners aged 62 and older, enabling them to access their home equity as cash while retaining ownership of their property and avoiding monthly mortgage payments.

This can provide financial support in retirement without the need to sell the home.

How do reverse mortgages work in Florida?

In Florida, reverse mortgages allow homeowners to convert their home equity into cash without the requirement of making monthly payments. This is provided they keep up with property maintenance and remain current on property taxes and insurance.

Who is eligible for a reverse mortgage in Florida?

Borrowers in Florida must meet certain criteria to qualify for a reverse mortgage: they should be 62 years of age or older, occupy the property as their primary residence, and possess complete ownership of the home or have only a small mortgage balance that can be paid off at closing.

What are the types of reverse mortgages available?

The three primary types of reverse mortgages available are Home Equity Conversion Mortgages (HECMs), proprietary reverse mortgages, and single-purpose reverse mortgages.

Each type offers different features and suitability depending on individual financial needs.

How are reverse mortgage funds typically used?

Reverse mortgage funds are typically utilized for home repairs, daily living expenses, medical bills, and long-term care needs. This flexibility allows homeowners to address significant financial obligations while maintaining their quality of life.