DSCR Loans for Investors

How To Calculate Your DSCR?

Calculate your DSCR by multiplying the NOI of your property by the debt service of your loan (as determined annually). Find your net profit based upon subtracting the reasonably necessary operating cost of your home from the gross rental income derived. Calculation of DSCR and NOI Debit Services. Keep in mind that the monthly rental income generated is a huge factor.

How to Analyze the Property in Florida for DSCR Loan?

Analyses for DSCR loans properties differ from preapproved loans in many respects. The lending company wants information about the potential for earning money. They are interested in information as follows:

Why are DSCR Loans Significant to Investors?

Also called investment property loans Non-QM loans, or rent-a-car loans, DSCR Loans, have become popular over the last few years. Why does everything seem to be happening? While conventional loans or money are available via the smaller banks, this financing can be complicated to qualify for and has large liquidity requirements. DSCR loans are designed to meet your professional investment needs. Let us examine this more carefully. DSCR loans are secured by the gross rents rather than the personal finances of its borrowers. Each commercial real estate and market is different but almost all investors like not having to produce tax returns, because their tax returns usually don’t show enough income on the tax returns.

How Do DSCR Loans in Florida Work?

DSCR loans or DSCR lending is a type of loan that has been developed to meet non-QM conditions and is offered to any real estate investor and property investors seeking financing. Non-QM loans are designed for homebuyers who do not have an established home loan history. In addition, other loans may have other incentives such as low monthly repayments that provide an alternative option for people who cannot afford their home loan. Loan Trust also offers borrowers with non-QM financing options including asset loans and bank statements. Does anyone need loans to get started? Tell me the answer. Get in touch with us. do we have borrowers eligible?

Potential Rental Income

When analyzing properties on an RDSR loan, it’s advisable to calculate rental income first. If a monthly rent amount of 12 months is multiplied by 12. Analyses of the annual rent income clearly showed how it could generate revenues.

What makes a good Debt Service Coverage Ratio?

A debt servicing coverage ratio of 1.5 or more is very good. If the DSCR ratio is one the rental is equal to the monthly payments of principal taxes, taxes, insurance fees and association fees if any.. A debt service insurance rating above 1 will help to subsidize PITIA. We have several different examples.

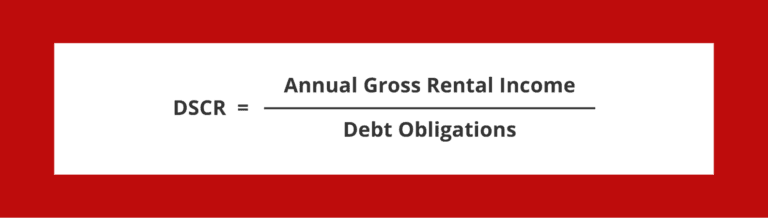

DSCR Loans formula: DSCR = NOI/Annual Debt Payments,

Where we enclose interest and other items such as income, expenses, interest and amortization. All year-long debt includes leased interest payments, along with capital repayments. For example, a DSCR of 1.75 if Mr. Lord wants an investment of $40,000. The Lord’s other real estate property produced 25 per cent more income than was necessary to service its debt obligations.

What Are Florida DSCR Loans?

DSCR loans provide an alternative to typical Florida home loans designed specifically by real estate investors. Rather than qualifying through income verification or employment history, you will qualify for loans by calculating a credit-return ratio. This ratio shows how much rent your home generates against the debts incurred annually in buying a rental home. DSCR loans offer a variety of conditions that aren’t for normal buyers. This loan is designed for property developers that want to invest in rental property but cannot buy a property owned for sale.

What to Look for in a DSCR Lender

Compare the different DSCR loans and lending companies. Find out which DSCR Lenders offer the lowest rates and that your property will fit their program.

Mortgage Terms

The longer the mortgage loan term is the better DSCR, because the lender has longer to repay it. In other words a property having a 30-year loan term with a 15-year loan term would have a higher DSCR if two of its properties had the similar NOI. This means that short term mortgages may result in lowered DSCRs. You may occasionally hear the term as service coverage ratio DSCR. It’s very rare to find a DSCR loan Florida Program with an adjustable rate mortgage.

How to Calculate the DSCR Loan for Buying Rental Property in Florida?

DSCR, is a measure that depicts the capability and ability of borrowers in making timely repayments. The loan balance is what the borrower has to pay back to the lending lender.

How Does DSCR Affect Loan Eligibility?

The DSCR is crucial when deciding whether to lend to borrowers or not. The high DSCR shows that the borrower will have excellent repayment capacities which make borrowers eligible. In comparison, a lower DSCR suggests borrowers could not repay their debt to income ratio, in time, which means the loan is not available to them.

Do You Need Proof of Income for a DSCR Loan?

Yes, proof of income is typically required for a DSCR (Debt Service Coverage Ratio) loan. Since DSCR loans typically are used to finance income-producing properties, the lender will want to ensure that the property can generate sufficient income to cover the loan payments. The lender will typically require documentation of the property’s net operating income (NOI), which is the income generated by the property after subtracting operating expenses.

DSCR Loan Property Types

Some common types of properties that may qualify for a DSCR loan include:

Commercial Properties: These are non-residential properties that are used for business purposes, such as office buildings, retail stores, warehouses, and industrial properties.

Multi-Family Residential Properties: These are residential properties with two or more units, such as apartment buildings, townhouses, and condominiums.

Mixed-Use Properties: These are properties that have both commercial and residential units, such as a building with retail stores on the ground floor and apartments above.

Hospitality Properties: These are properties that provide lodging and other services to guests, such as hotels, motels, AirBNB and resorts.

Healthcare Properties: These are properties that provide medical and healthcare services, such as hospitals, clinics, and assisted living facilities.

Special Use Properties: These are properties that have unique or specialized uses, such as schools, churches, and recreational facilities.

Overall, the property must have a history of stable occupancy and positive cash flow to be considered for a DSCR loan. The lender will also consider the borrower’s qualifications and financial strength to ensure that they can manage the property and repay the loan. The specific property types that may qualify for a DSCR loan may vary depending on the lender and the market conditions.

Debt Service

Debt service refers to the amount of money required to make regular debt service payments on a debt, such as a loan or bond. Debt service includes both principal and interest payments and is typically calculated as a fixed amount that must be paid on a regular basis, such as monthly, quarterly, or annually. The debt service amount is determined by the terms of the loan or bond, including the interest rate, repayment period, and payment schedule. In the context of a business or investment property, the debt service is an important factor in determining the property’s cash flow and profitability, as it represents a fixed expense that must be paid before any profits can be realized. This is the debt service coverage ratio.

What Are the Requirements for a DSCR Loan in Florida?

The underwriting requirements for a Debt Service Coverage Ratio or a DSCR loans are generally similar to those in other states. However, there may be some specific requirements or guidelines that are unique to Florida. Some of the common underwriting requirements for a DSCR loan in Florida include:

Debt Service Coverage Ratio (DSCR): As mentioned earlier, the DSCR is a key factor in underwriting a DSCR loan. In Florida, lenders typically require a minimum DSCR of 1.20 to 1.25 for commercial properties and 1.15 to 1.20 for multi-family residential properties.

Loan-to-Value Ratio (LTV): The LTV ratio is another important underwriting requirement for a DSCR loan. In Florida, lenders typically require an LTV of no more than 75% to 80% for commercial properties and 80% to 85% for multi-family residential properties.

Property Type: In Florida, DSCR loans are typically available for commercial and multi-family residential properties. The property must have a history of stable occupancy and cash flow.

Borrower Qualifications: Lenders in Florida will also consider the borrower’s creditworthiness, experience in managing similar properties, and financial strength. A minimum credit score may be required, and borrowers must demonstrate a successful track record of property management.

Property Condition: The property must be in good condition and meet local building codes and zoning requirements. Lenders may require a property inspection and appraisal to verify its condition and value.

Insurance Requirements: In Florida, lenders may require that the property be insured against hurricanes, floods, and other natural disasters.

It’s important to note that these underwriting requirements may vary depending on the lender and the specific circumstances of the loan. It’s always a good idea to consult with a qualified lender or financial advisor to understand the requirements and options available for a DSCR loan.

Terms

What are the lenders rate and fees?

This information should be accompanied by an accurate price list and should give you an estimate of the cost of purchase loans. It would be a shame if you had to leave with unexpected expenses. Almost every lender has an origination fee and administrative fee (invoice fee and documentation fee). Real estate investors love these loans although the rates are higher.

They come with faster application and closing times

DSCR loans typically have an efficient quick application process because no personal documents are required. This is often a necessity for real estate investors. Keep in mine they buy investment properties to grow their real estate investment portfolio.

Lenders don’t consider personal income

The fact that most DSCR lenders‘ loans don’t take into account personal data is much easier for borrowers who may not need a lot of cash. However, this will vary based on the DSCR lenders and what the monthly payment will be since some real estate lenders don’t want higher mortgage payments.

What is the Minimum DSCR to Qualify for the DSCR Loan Florida?

Most lenders recommend an DSCR of 1. The DSCR is an important factor lenders take into consideration when granting the loan because they understand whether they are able to repay the monthly loan required by the lender’s loan terms. Lenders feel confident that their loan will generate 25% of monthly debt payments from its total earnings. If a home’s monthly loan payment is $1,000, a loan is guaranteed that it will repay that debt by generating at least $15,000 in income. If you want an enormous loan amount it is necessary that you pay 1.4 for the loans. Please remember that.

Pros and Cons of DSCR Loans

The other loan based, option has grew in popularity in recent times because it uses rental income as opposed to personal income to determine the eligibility for the loans. It is easy to qualify for than banks or agencies loans and is cheaper than cash loans for investment in property purchases. However these loans have drawbacks. One of the things that can impact qualifying for a DSCR loan program is high property taxes.

Is the lender focused on and experienced in working with investors?

We find it to be the most crucial aspect. Lenders working on investor projects often recognize the facets of finance and develop programs tailored to the requirements of the investor. DSCR loans are becoming very popular. Here is a list of ways to improve your experience with an established lender.

What Are the Requirements for a DSCR Loan in Florida?

If you wanted a traditional loan as oppose to a DSCR loan, the lender would need your paycheck, bank statement and your credit history proofs. DSCR loans for Florida can only be obtained by calculating DSCRs on your rental properties and applying the same for loans. The minimum rental income DSCR is one means if your rental income is at least $1.50, the annual debt for the property can be easily repaid. If you apply for a DSCR credit from Griffin funding, you will require an additional down payment, usually between 30% and 40%. The credit limit must be minimal.

Overall, the underwriting requirements for a DSCR loan are designed to ensure that the property can generate sufficient cash flow to repay the loan and that the borrower is financially qualified and capable of managing the property effectively.

What Is a Good DSCR?

DSCRs must be deposited in the state for a loan to be eligible for a Florida loan. As your DSCR gets higher, the more rent you must pay for it. A good DSCR may provide better terms and reduced down payment rates as well as fewer interest rates for customers. In Florida, Loan Trust offers low-interest credit scores that range from 0.75 to 1.75.

Compare Rates from DSCR Lenders

Make a prequalified offer on Investor Cashflow mortgages if the property demonstrates potential rental income.

Loan-To-Value Ratio

This final step determines the ratio of loans to values. It is done by dividing loan amounts by property value. LTV measures the degree of risk on an asset. Typically borrowers with a higher value of property will get more interest and risky loans. DSCR loans require much more time for analysis of properties, making this a good investment for the investor.

Mortgage Rate

Higher mortgage rates will increase the DSCR, increasing the need for service of the debts. Nevertheless, lower rates on home loans could affect DSCR borrower’s ability. For instance – When 2 Florida homes have identical nominated mortgage terms and the same mortgage terms, the other property has an interest rate of 6.7% versus the property has an interest rate of 4%, this property would have a better DSCR. As of September 2022 DSCR loans with 25% down payments and 1.2 DSCR % have DSCR loan rates of 7.732%.

Is it hard to get a DSCR loan?

DSCR loans are made based on cash flow of your property making qualification more convenient for applicants. Once approved by your lender, it may be more difficult to get approved for conventional loan. Besides, applications can be faster streamlined and DSCR Loan applications are generally less rigorous than other financings compared to a dscr loan.

Borrower types

Typically a landlord or investor will finance properties within a company and this lend has its own peculiarities in itself. In some cases entity documentation is required. It is just another way to get more information about DSCR Mortgages. Visio Lending has been mastering the niche market for more than 10 years and the loan originated over $22bn and included over 641m of vacation rental. Learn more about DSCR loans at Wikipedia.

Associated Fees

In addition, the fees for loan can decrease the debt service coverage ratio (DSCR). This includes origination costs, appraisal costs and closing costs. This increases total interest rate and increases the debt service required in the payment. When looking at loan applications you need to compare the DSCRs of various lenders. This will help you determine what loan provider offers a best deal. The best way to do this is by using debt service insurance ratio calculator. So it makes sense to get a great loan.

What are the interest rates on a DSCR loan?

The DSCR rate is 7.722% on 30-year Fixed Loans with 50% down and a 1.