DSCR loan Michigan: Private Lender DSCR Loans

How does the DSCR Loan work for property owners? What are their benefits? The guide below is the most comprehensive guide to lenders offering DCR loans for students in Michigan. This comprehensive guide explains the process for applying for DSCR loan and compares lenders offering DSCR loans in Michigan. This comprehensive guide is designed to assist real estate investors in choosing the best lending institution. So, we’ll show you how to get approved for a DSCR loan program in Michigan.

No Tax Returns Required for Michigan Real Estate Investors

DSCR loans offer borrowers with no property tax obligation to file their financial reports and make it an accessible financing solution for securing investments in commercial properties.

Benefits of Michigan DSCR Loans

Getting the right loan is very crucial. Michigan’s debt service coverage ratio loans are one of the most attractive loan available. Get started now and get an accurate estimate today! Please submit your application today.

Variety of Lenders

Various lenders offer loan amount for DSCR lending to property investors in Michigan. It will help them find the best solution. If you want your DSCR loan in Michigan, please contact Loan Trust so we can help with any mortgage loan questions.

Find the Best DSCR Lender in Michigan

Become eligible for an Investor Cash Flow Loan for rentable income.

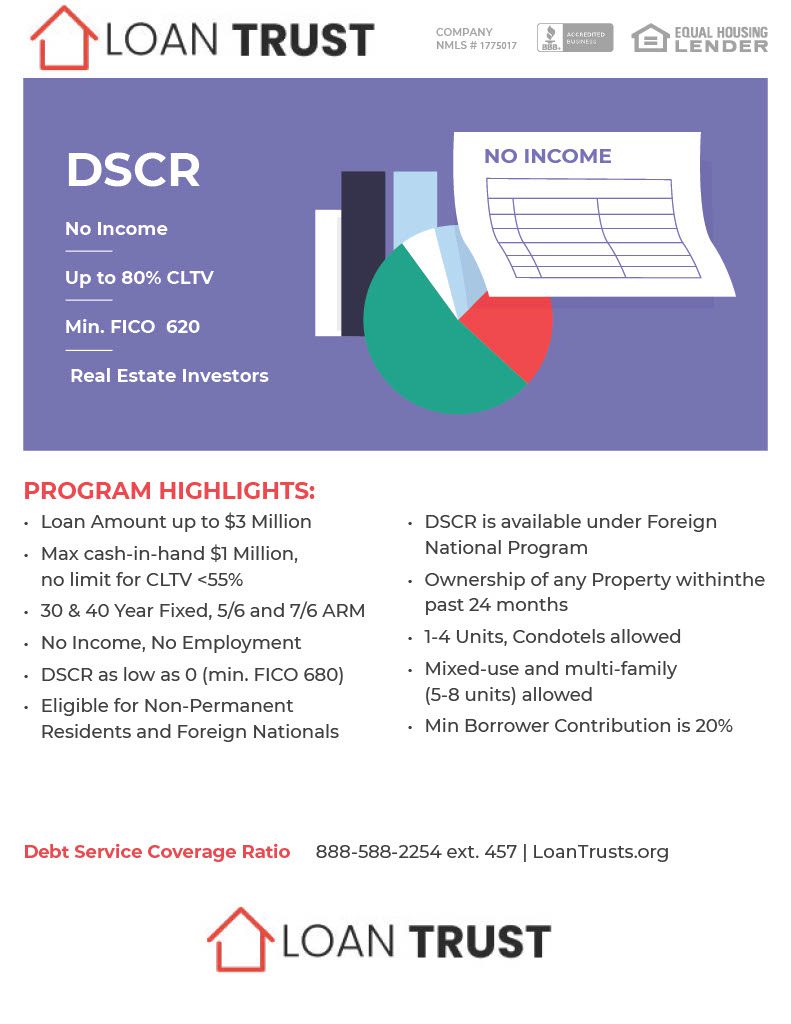

Michigan DSCR Eligibility Requirements

Applicants who apply with Michigan DSCR need at least an DSCR above the required threshold for the loan. Different lenders are required to have different DSCR calculation requirements but it must always happen unless the borrower wants it to happen. The minimum credit scores and down payments required for a secured loan must also include the DSCR threshold. We require a 20% deposit and a bigger deposit is required to lower our DSCR ratio. Although some DSCR lending is required, these requirements are very flexible. DSCR loans are good alternatives in Michigan.

Eligibility Criteria and Loan Terms for DSCR Loans Michigan

DSCR loans in Michigan have certain criteria everyone must meet. Here are the requirements for borrowing. The property must have sufficient income to cover the debt is the most important factor.

DSCR Loan in Michigan Requirements

See current rate of interest on DSCR loans.

Prepayment Penalties

In Michigan, payday loans are subject to payment penalties. The penalty can be between 10% and 3% and is applicable in situations of late repayment or late payment. These penalties protect the lenders who have repaid the loans on time from possible loss. In most situations refundable payment penalties are refunded when an applicant refinances traditional loans or sells the investment property within one business day of the expiration.

Steps to Get DSCR Loans in Michigan

This guide describes the process for applying for DSCR loans from Michigan. Please consult one of our Loan Officers for a DSCR Loan or to get more information.

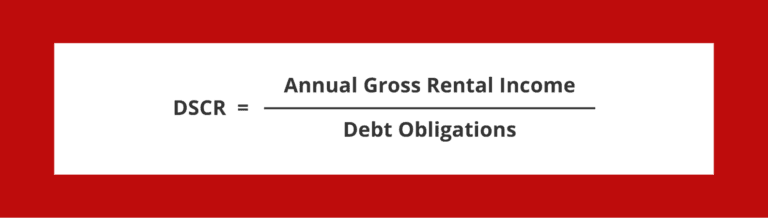

What Is the Importance of DSCR for Real Estate Investment Loans?

DSCR, debt service coverage ratios, is a measure of rental income versus annual loan debt. When you have rent income that is above the amount that you have to repay each month, it can show that your borrower’s creditworthiness and rating is good. Lenders offer loans geared toward buying rental properties that can help pay your monthly loans. DSCRs are calculated by measuring the rent that’s taxable or higher. Almost all lending institutions require you to meet the DSCR to qualify for loans, although these numbers vary from bank to bank and are generally the same.

Terms of DSCR Loans Michigan

DSCR loans in Michigan provides property investment property investors with an innovative financing solution. Learn more about Michigan loans and their coverage rates.

Repayment Periods & Interest Rates

DSCR loan programs typically offer 30-year terms. Although interest rates on these loans are variable, they can vary depending on several factors. Most loans with DSCR have interest rates up to 1-2% above typical lending rates. Check latest DSCR Loans Rates on our site! If you’ve got an DSCR loan in Michigan, Home

Compare Rates from Best DSCR Lenders

Make sure investors have cash flow loans pre-qualified based on rental income.

Loan Trust has an enormous network of lenders.

What is the minimum DSCR ratio requirement for getting a DSCR loan in Michigan?

A. The credit score for a DSCR Loan in Michigan should be 600 or better. Some lenders will accept your DSCR loan with a lower credit score, but the down payment and interest maybe higher.

How Does a DSCR Loan Work?

Understanding how loan servicing coverage ratios work is a very important first step. The DSCR loan reflects non-QM borrowing and is a conventional loan that has less restrictive requirements and approved procedures than the conventional mortgage. Non-QM loan programs can serve a wide range of customers, from individuals to property investors to individuals with high incomes. The Non-QM lending system provides alternative conditions that can be easily approved. Contrary to other non-QM types such as asset-based loans, recent credit events loans, and bank statement loans, DSCR loans specifically target real property investors.